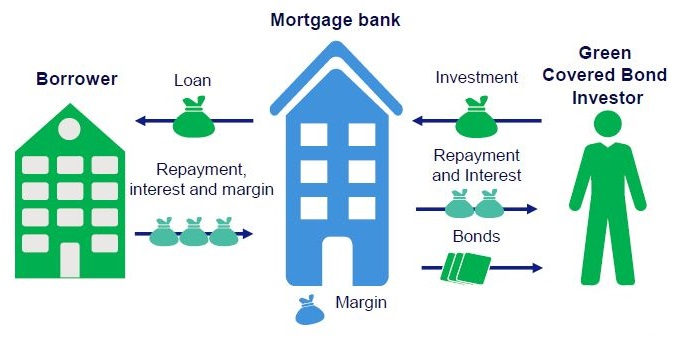

Rikard, you closely followed the work on the Taxonomy both at EU and Swedish levels, why and how the Taxonomy is relevant for the real estate sector? Which part of the sector is primarily targeted?

The Taxonomy can be described as a classification system for companies and investors to determine whether an economic activity is “environmentally sustainable”. The real estate sector is obviously not only closely linked to the finance sector and investors, it is also a vital part of the economy and it plays a key role in the transition towards more sustainability. Although, it does not affect individuals and their credit directly, the Taxonomy should also set a benchmark in the covered bond and green mortgage bond markets and ultimately affects the mortgage credit market. For our sector, construction of new buildings, renovation of existing buildings and acquisition and ownership of buildings are the most relevant economic activities classified in the Taxonomy.